Financial Analyst Warns Of Event Unable To Recover From

Latest on the current financial crisis and the coming economic crash

“Things are breaking down, something big is happening,” according to leading alternative news web site SGT Report. Citing the recent emergency meeting between the Federal Reserve and President Obama, America’s explicit warning to other countries not to devalue their currencies against the dollar, and scores of other global indicators, SGT Report’s latest interview with Bill Holter may be your last chance to get ready for the next wave. What we’re looking at is an event that you’re not going to be able to recover from…

If this market snaps and the markets close and you’re not in position, you’re out for the rest of your life. That an economic catastrophe is imminent should be at the very forefront of mainstream news. But instead of heeding the warnings, the propaganda has gone so deep that even President Obama says that those who say there is something wrong are peddling fiction. But the reality is that even they know what’s coming. The following exchange between SGT and guest Bill Holter is all you really need to know: READ MORE

Current Economic Collapse News Brief

World Economic Collapse will be SUDDEN and by summer, Gold over $2000?

Gerald Celente - Trends In The News - "Retail Sales Down, Worst Yet To Come?"

The Economy: “Goldman Sachs ‘Bail-in’ Plot Designed to Steal Your Bank Account”

“Goldman Sachs ‘Bail-in’ Plot Designed to Steal Your Bank Account”

by Dave Hodges

“Bail-outs, Bail-ins, the average

consumer has trouble keeping these terms and their meanings straight.

Both terms are relatively new on the American economic scene. Here is what these terms mean:

“A bail-out is when outside

investors rescue a borrower by injecting money to help service a debt.

Bail-outs of failing banks in Greece, Portugal and Iceland were

primarily financed by taxpayers.

A bail-in occurs when the

borrower’s creditors are forced to bear some of the burden by having a

portion of their debt written off. For example, bondholders in Cyprus

banks and depositors with more than 100,000 euros in their accounts were

forced to write-off a portion of their holdings. This approach

eliminates some of the risk for taxpayers by forcing other creditors to

share in the pain and suffering.”

As an American investor, if given no

choice, I would prefer a bail-out over a bail-in. In the case of a

bail-in, it is my money that is being stolen from me by the bankers to

they can keep their institution afloat as opposed to the bail-in where

it is my money that is directly taken from me in order to satisfy

bankers debts.

Goldman Sachs Is Covertly Ushering In Bail-Ins Beneath the Radar: Goldman

Sachs has a new new online bank that it acquired from General Electric

Co. The evidence is quite clear that Goldman Sachs has taken the lead in

what will become the “the Great American rip-off”, which will lead to

massive bail-ins around the country. Before we go further in this

developing story in which bail-ins are already happening in America,

let’s take a look at the character of Goldman Sachs in order to gain

some much needed perspective on who will be setting the trend in this

newest waves of the bankers hijacking the country.

Goldman Sachs and Integrity Are Mutually Exclusive Terms: If

one wants to predict the next false flag attack, one merely has to

watch the actions and the money movements of Goldman Sachs. In the days

leading up to the attacks on 9/11, Goldman Sachs “shorted” the sale of

airline stocks which plummeted in the aftermath of the attacks. Just a

coincidence you say? In the days leading up to the housing bubble,

Goldman Sachs shorted housing stocks which ignited the bubble. The

Federal government fined Goldman Sachs, but in typical fashion, nobody

went to jail. Just another coincidence you say?

As I documented in my seven part

series, “The Great Gulf Coast Holocaust,” Goldman Sachs executed a “put

option” for preferred insiders invested in Transocean stock,thus

protecting the profits of these preferred insiders on the morning of the

explosion. Transocean was the owner of the ill-fated oil rig. Goldman

Sachs also sold the lion’s share of its BP stock less than two weeks

before that fateful day on April 20, 2010. Nalco was the subsidiary of

Goldman Sachs and BP at the time of the explosion. Who is Nalco? Nalco

was the exclusive manufacturer of the deadly oil dispersant, Corexit.

Corexit has done more to wreck the ecology of the Gulf as well as the

health of the Gulf Coast residents than the oil spill itself. Again,

this is all documented in my seven part series. By the way, I count

another three coincidences in this paragraph alone and if you are

keeping score, we are looking at a total of five amazing coincidences.

But wait, there is more!

The moral of this story is clear, if

there is to be a significant false flag event, the financial actions of

Goldman Sachs will prove to be the key. And Goldman Sachs’ actions have

signaled yet another oncoming false flag. As I reported on in April of

2013, Goldman Sachs instructed its brokers to sell short on gold stocks.

And then after the bulk of the gold market panicked and the price of

gold plummeted in a massive sell off, the Goldman Sachs boys did it

again. The Goldman Sachs brokers began to purchase gold in massive

amounts, for its elite clients, at a greatly depressed price. By the

way, Goldman Sachs employed the EXACT same strategy with regard to the

Gulf Oil tragedy. When Goldman Sachs sold off BP stock in the days

before the explosion, they purchased massive amounts of BP stock at a

greatly reduced price in June of 2010. In short (no pun intended),

Goldman Sachs is clearly a criminal enterprise organization.

Any financial endeavor that Goldman Sachs is involved in should be looked at with a wary eye.

Goldman Sachs Will Lead the Way in the Covert Theft of Your Money: In a major transaction that went virtually unnoticed, Goldman Sachs just took over $16 billion of deposits from the online business it bought from GE Capital.

Goldman Sachs immediately merged this platform with its GS Bank USA and

created a hybrid banking model. Goldman Sachs is offering 1.05 percent

interest on savings accounts that are opened online. The bank has added

to its deposit base by 700%.

Here is where the Goldman actions get very interesting and very serious. On this past Tuesday, two U.S. agencies have announced

their special version of a long-term liquidity rule outlined by global

regulators in 2014. When we start reading professional sounding catch

phrases, it is time to clutch our collective wallets as Goldman

announces that it is embracing the “funding ratio” policy that requires

banks to hold enough easy-to-sell assets to meet any liabilities coming

due in the next 12 months. The easy to sell assets are your bank account.

New Rules: Hoping you will get

lost in the words, Goldman is planning to rob you blind. Under these new

policies, deposits are viewed as a more stable form of financing than

market-based sources such as repossessions.

Goldman Sachs said in its latest

annual report that it’s already in full compliance with the pending

short-term rule, called the liquidity coverage ratio. The term, the

liquidity coverage ratio means that your deposits are the source of

backing for the banks instead of the U.S. taxpayer. However, the only

way that could be achieved is if the FDIC is not involved. And for the

FDIC to not be involved, your bank assets could not be counted as money.

I wrote an article in November of 2014

in which I stated that your money had been stolen. Why would I make

such an outrageous claim? Because at the G20 conference held at that

time in Brisbane, Australia, it was decided that a depositor’s assets

would no longer be called money when it went into the bank. This became

the impetus for shifting the backing of banks away from bail-outs to

bail-ins where your deposit can be confiscated by the bank at any time

and in any amount.

Conclusion: Who else but Goldman Sachs would be the one to usher in a brand new way to steal American citizens’ money?”

Economic Markets Shake As Fiat Currencies Collapse; Earthquakes Everywhere Too

http://beforeitsnews.com/politics/2016/04/economic-markets-shake-as-fiat-currencies-collapse-earthquakes-everywhere-too-2797700.html

For Stan Druckenmiller This Is "The Endgame" - His Full 'Apocalyptic' Presentation

Several days ago, hedge fund legend Stan Druckenmiller spoke at the Sohn Conference, delivering what may have been his most bearish fire and brimstone sermon yet, and in fact according to some buysiders who were present, its somber mood and lack of faux optimism was downright apocalyptic. And how can it not be when Druckenmiller said that while the Fed and policymakers have no endgame, markets do - hinting that one is rapidly approaching - and suggested that everyone should liquidate their equity holdings and buy a certain 5000 year old shiny asset, which as we reported earlier this week, is Druckenmiller's "largest currency allocation."And just so everyone can appreciate what is keeping up at night one of the most illustrious investing minds of any generation (with a 30% average return from 1986 through 2010) below we repost his entire presentation delivered at the May 4 Sohn Conference, titled appropriately enough...

* * *

The Endgame

When I started Duquesne in February of 1981, the risk free rate of return, 5 year treasuries, was 15%. Real rates were close to 5%. We were setting up for one of the greatest bull markets in financial history as assets were priced incredibly cheaply to compete with risk free rates and Volcker’s brutal monetary squeeze forced much needed restructuring at the macro and micro level. It is not a coincidence that strange bedfellows Tip O’Neill and Ronald Reagan produced the last major reforms in social security and taxes shortly thereafter. Moreover, the 15% hurdle rate forced corporations to invest their capital wisely and engage in their own structural reform. If this led to one of the greatest investment environments ever, how can the mirror of it, which is where we are today, also be a great investment environment? Not a week goes by without someone extolling the virtues of the equity market because “there is no alternative” with rates at zero. The view has become so widely held it has its own acronym, “TINA”.

Not only valuations were low back in 1981 but financial leverage was less than half of what it is today. The capacity of credit inspired growth was still ahead of us. The policy response to the global crisis was, and more importantly, remains so forceful that it has prevented any real deleveraging from happening. Leverage has actually increased globally. Ironically from where I stand, that has been the intended goal of most policymakers today.

Let me focus on two of the main policies that have not only prevented a clean-up of past excesses in developed markets but also led to an explosion in leverage in Emerging markets. The first of these policies has been spearheaded by the Federal Reserve Bank in the US. By most objective measures, we are deep into the longest period ever of excessively easy monetary policies. During the great recession, rates were set at zero and they expanded their balance sheet by $1.4T. More to the point, after the great recession ended, the Fed continued to expand their balance sheet another $2.2T. Today, with unemployment below 5% and inflation close to 2%, the Fed’s radical dovishness continues. If the Fed was using an average of Volcker and Greenspan’s response to data as implied by standard Taylor rules, Fed Funds would be close to 3% today. In other words, and quite ironically, this is the least “data dependent” Fed we have had in history. Simply put, this is the biggest and longest dovish deviation from historical norms I have seen in my career. The Fed has borrowed more from future consumption than ever before. And despite the US global outperformance, we currently have the most negative real rates in the G-7. At the 2005 Ira Sohn Conference, looking at a more muted but similar deviation, I argued that the Greenspan Fed was sowing the seeds of an historical housing bubble fed by reckless sub-prime borrowing that would end very badly. Those policy excesses pale in comparison to the duration and extent of today’s monetary experiment

The obsession with short-term stimuli contrasts with the structural reform mindset back in the early 80s. Volcker was willing to sacrifice near term pain to rid the economy of inflation and drive reform. The turbulence he engineered led to a productivity boom, a surge in real growth, and a 25 year bull market. The myopia of today’s central bankers is leading to the opposite, reckless behavior at the government and corporate level. Five years ago, one could have argued it was in search of “escape velocity.” But the sub-par economic growth we are experiencing in the 8th year of a radical monetary experiment and in Japan after more than 20 years has blown that theory out of the water. And smoothing growth over a cycle should not be confused with consistently attempting to borrow consumption from the future. The Fed has no end game. The Fed’s objective seems to be getting by another 6 months without a 20% decline in the S&P and avoiding a recession over the near term. In doing so, they are enabling the opposite of needed reform and increasing, not lowering, the odds of the economic tail risk they are trying to avoid. At the government level, the impeding of market signals has allowed politicians to continue to ignore badly needed entitlement and tax reform.

Look at the slide behind me. The doves keep asking where is the evidence of mal-investment? As you can see, the growth in operating cash flow peaked 5 years ago and turned negative year over year recently even as net debt continues to grow at an incredibly high pace. Never in the post-World War II period has this happened. Until the cycle preceding the great recession, the peaks had been pretty much coincident. Even during that cycle, they only diverged for 2 years, and by the time EBITDA turned negative year over year, as it has today, growth in net debt had been declining for over 2 years. Again, the current 5-year divergence is unprecedented in financial history!

And if this wasn’t disturbing enough, take a look at the use of that debt in this cycle. While the debt in the 1990’s financed the construction of the internet, most of the debt today has been used for financial engineering, not productive investments. This is very clear in this slide. The purple in the graph represents buybacks and M/A vs. the green which represents capital expenditure. Notice how the green dominates in the 1990’s and is totally dominated by the purple in the current cycle. Think about this. Last year, buybacks and M&A were $2T. All R&D and office equipment spending was $1.8T. And the reckless behavior has grown in a non-linear fashion after 8 years of free money. In 2012, buybacks and M&A were $1.25T while all R&D and office equipment spending was $1.55T. As valuations rose since then, R&D and office equipment grew by only $250b, but financial engineering grew $750b, or 3x this! You can only live on your seed corn so long. Despite no increase in their interest costs while growing their net borrowing by $1.7T, the profit share of the corporate sector peaked in 2012. The corporate sector today is stuck in a vicious cycle of earnings management, questionable allocation of capital, low productivity, declining margins, and growing indebtedness. And we are paying 18X for the asset class.

A second source of myopic policies is now coming from China. In response to the global financial crisis, China embarked on a $4 trillion stimulus program. However, because they had engaged in massive infrastructure investment the previous 10 years, and that was the primary stimulus pipe they chose; this only aggravated the overcapacity in the investment side of their economy. Not surprisingly, this only provided a short term pop in nominal growth. While we were worried about bank assets to GDP in 2012, incredibly, credit has increased by 70% of GDP in the 4 years since then. Just to put this in perspective, this means that since 2012 the Chinese banking sector has allowed credit to grow by the amount of the entire Brazilian GDP per year! Picture the entire Brazilian production in new houses and infrastructure. Incredibly, all this credit growth has been accompanied by a fall in nominal GDP growth from 15% to 5%. This is an extremely toxic cocktail for companies that have borrowed at 10% expecting 15% sales growth. Our strong suspicion therefore is that a large part of this growth is just credit flowing to otherwise insolvent borrowers. How else to explain the lack of NPL problem in heavy industries hit by lower prices and sales growth?

As a result, unlike the pre-stimulus period, when it took $1.50 to generate a $1.00 of GDP, it now takes $7. This is extremely rare and dangerous. The most recent historical analogue was the U.S. in the mid- 2000’s when the debt needed to generate a $ of GDP increased from $1.50 to $6 during the subprime mania. Two years ago, we had hope the Chinese were ready to accept a slowdown in exchange for reform. Unfortunately, with the encouragement of the G-7, they have opted for another investment focused fiscal stimulus which may buy them some time but will exacerbate their problem. They do not need more debt and more houses.

As the chart shows, this will remove a major cylinder from the engine of world growth.

I have argued that myopic policy makers have no end game, they stumble from one short term fiscal or monetary stimulus to the next, despite overwhelming evidence that they only produce an ephemeral sugar high and grow unproductive debt that impedes long term growth. Moreover, the continued decline of global growth despite unprecedented stimulus the past decade suggests we have borrowed so much from our future for so long the chickens are coming home to roost. Three years ago on this stage I criticized the rationale of fed policy but drew a bullish intermediate conclusion as the weight of the evidence suggested the tidal wave of central bank money worldwide would still propel financial assets higher. I now feel the weight of the evidence has shifted the other way; higher valuations, three more years of unproductive corporate behavior, limits to further easing and excessive borrowing from the future suggest that the bull market is exhausting itself.

If we have borrowed more from our future than any time in history and markets value the future, we should be selling at a discount, not a premium to historic valuations. It is hard to avoid the comparison with 1982 when the market sold for 7x depressed earnings with dozens of rate cuts and productivity rising going forward vs. 18x inflated earnings, productivity declining and no further ammo on interest rates.

The lack of progress and volatility in global equity markets the past year, which often precedes a major trend change, suggests that their risk/reward is negative without substantially lower prices and/or structural reform. Don’t hold your breath for the latter. While policymakers have no end game, markets do.

On a final note, what was the one asset you did not want to own when I started Duquesne in 1981? Hint…it has traded for 5000 years and for the first time has a positive carry in many parts of the globe as bankers are now experimenting with the absurd notion of negative interest rates. Some regard it as a metal, we regard it as a currency and it remains our largest currency allocation.

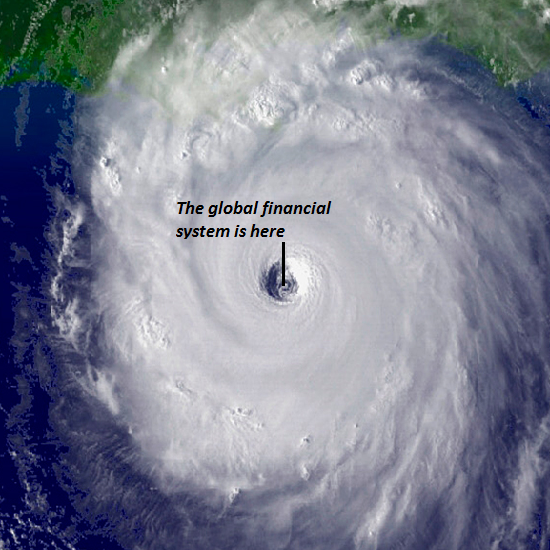

We're In The Eye Of A Global Financial Hurricane

The only "growth" we're experiencing are the financial cancers of systemic risk and financialization's soaring wealth/income inequality.The Keynesian gods have failed, and as a result we're in the eye of a global financial hurricane.

The Keynesian god of growth has failed.

The Keynesian god of borrowing from the future to fund today's consumption has failed.

The Keynesian god of monetary stimulus / financialization has failed.

Every major central bank and state worships these Keynesian idols:

1. Growth. (Never mind the cost or what kind of growth--all growth is good, even the financial equivalent of aggressive cancer).

2. Borrowing from the future to fund today's keg party, worthless college diploma, particle board bookcase, stock buy-back, etc. (oops, I mean "investment")--a.k.a. deficit spending which is a polite way of saying this unsavory truth: stealing from our children and grandchildren to fund our lifestyles today.

3. Monetary stimulus / financialization. If private investment sags (because there are few attractive investments at today's nosebleed valuations and few attractive investments in a global economy burdened with massive over-production and over-capacity), drop interest rates to zero (or below zero) to "stimulate" new borrowing... for whatever: global carry trades, bat guano derivatives, etc.

Here is my definition of Financialization:

Financialization is the mass commodification of debt and debt-based financial instruments collaterized by previously low-risk assets, a pyramiding of risk and speculative gains that is only possible in a massive expansion of low-cost credit and leverage.

That is a mouthful, so let's break it into bite-sized chunks.

Home mortgages are a good example of how financialization increases financial profits by jacking up risk and distributing it to suckers who don't recognize the potential for staggering losses.

In the good old days, home mortgages were safe and dull: banks and savings and loans institutions issued the mortgages and kept the loans on their books, earning a stable return for the 30 years of the mortgage's term.

Then the financialization machine revolutionized the home mortgage business to increase profits. The first step was to generate entire new types of mortgages with higher profit margins than conventional mortgages. These included no-down payment mortgages (liar loans), no-interest-for-the-first-few-years mortgages, adjustable-rate mortgages, home equity lines of credit, and so on.

This broadening of options (and risks) greatly expanded the pool of people who qualified for a mortgage. In the old days, only those with sterling credit qualified for a home mortgage. In the financialized realm, almost anyone with a pulse could qualify for an exotic mortgage.

The interest rate, risk and profit margins were all much higher for the originators. What's not to like? Well, the risk of default is a problem. Defaults trigger losses.

Financialization's solution: package the risk in safe-looking securities and offload the risk onto suckers and marks. Securitizing mortgages enabled loan originators to skim the origination fees and profits up front and then offload the risk of default and loss onto buyers of the mortgage securities.

Securitization was tailor-made for hiding risk deep inside apparently low-risk pools of mortgages and rigging the tranches to maximize profits for the packagers at the expense of the unwary buyers, who bought high-risk securities under the false premise that they were "safe home mortgages."

Financialization-- which can only expand to dominate an economy if it is supported by a central bank bent on expanding credit--has two inevitable and highly toxic consequences:

-- Risk seeps into every nook and cranny of the financial system, greatly increasing the odds of a systemic domino reaction in financial meltdowns. This is precisely what we saw in the 2008-09 Global Financial Meltdown (GFM): supposedly "contained" subprime mortgages toppled dominoes left and right, bringing the entire risk-saturated system to its knees.

-- Extraordinary wealth and income inequality, as those closest to the central bank money/credit spigots can scoop up income-producing assets first at much lower costs than Mom and Pop Main Street investors.

The rising anger of the masses left behind by the central bank / financialization wealth harvesting machine is the direct result of Keynesian monetary stimulus that rewards debt-based speculative gambles by those closest to the cheap-credit spigots.

As I explain in my book Why Our Status Quo Failed and Is Beyond Reform, the only possible output of central bank monetary stimulus is financialization, and the only possible output of financialization is unprecedented wealth and income inequality.

The global financial system is in the eye of an unprecedented hurricane. While central bankers are congratulating themselves on their god-like mastery of Nature, and secretly praying to the idols of the Keynesian Cargo Cult every night, the inevitable consequence of borrowing from the future, the obsession with "growth" at any cost and financialization /monetary stimulus, a.k.a. the rich get richer thanks to central banks is systemic collapse.

Don't fall for the mainstream media and politicos' shuck-and-jive that all is well and "growth" will return any day now. The only "growth" we're experiencing are the financial cancers of systemic risk and financialization's soaring wealth/income inequality.

When The Economy Collapses It Will Be Fast And Hard: V The Guerrilla Economist

Financial Collapse Leads To War – Gerald Celente and Stefan Molyneux

What is the state of the world economy – and what does the future hold? Gerald Celente joins Stefan Molyneux to discuss the growing wealth gap in the United States, the rise of negative interest rates, out of control central banks, the Military Industrial Complex, the fall of the political establishment, housing market trends, the role of China, stagflation in Japan, fiat currency wars, replacing income tax with tariffs and how economic collapse often leads to war!Gerald Celente is the head of the Trends Research Institute and the publisher of The Trends Journal – earning a reputation as “today’s most trusted name in trends” for accurate and timely forecasts. To subscribe to the Trends Research journal, please go to:http://www.trendsresearch.com

Collapse of the Western Fiat Monetary System May Have Begun. China, Russia and the Reemergence of Gold-Backed Currencies

By Peter Koeing

On 19 April 2016, China was rolling

out its new gold-backed yuan. Russia’s ruble has been fully supported by

gold for the last couple of years. Nobody in the western media talks

about it. Why would they? – A western reader may start wondering why he

is constantly stressed by a US dollar based fiat monetary systems that

is manipulated at will by a small elite of financial oligarchs for their

benefit and to the detriment of the common people.

In a recent Russia Insider article, Sergey

Glaziev, one of Russia’s top economists and advisor to President Putin

said about Russia’s currency, “The ruble Is the most gold-backed

currency in the world”. He went on explaining that the amount of rubles

circulating is covered by about twice the amount of gold in Russia’s

Treasury.

In

addition to a financial alliance, Russia and China also have developed

in the past couple of years their own money transfer system, the China

International Payment System, or the CIPS network which replaces the

western transfer system, SWIFT, for Russian-Chinese internal trading.

SWIFT, stands for the Society for Worldwide Interbank Financial

Telecommunication, a network operating in 215 countries and territories

and used by over 10,000 financial institutions.

In

addition to a financial alliance, Russia and China also have developed

in the past couple of years their own money transfer system, the China

International Payment System, or the CIPS network which replaces the

western transfer system, SWIFT, for Russian-Chinese internal trading.

SWIFT, stands for the Society for Worldwide Interbank Financial

Telecommunication, a network operating in 215 countries and territories

and used by over 10,000 financial institutions.

Up

until recently almost every international monetary transaction had to

use SWIFT, a private institution, based in Belgium. ‘Private’ like in

the US Federal Reserve Bank (FED), Wall Street banks and the Bank for

International Settlements (BIS); all are involved in international

monetary transfers and heavily influenced by the Rothschild family. No

wonder that the ‘independent’ SWIFT plays along with Washington’s

sanctions, for example, cutting off Iran from the international transfer

system. Similarly, Washington used its arm-twisting with SWIFT to help

Paul Singer’s New York Vulture Fund to extort more than 4 billion

dollars from Argentina, by withholding Argentina’s regular debt payments

as was agreed with 93% of all creditors. Eventually Argentina found

other ways of making its payments, not to fall into disrepute and

insolvency.

All of this changed for Argentina, when

Mauricio Macri, the new neoliberal President put in place by Washington,

appeared on the scene last December. He reopened the negotiations and

is ready to pay a sizable junk of this illegal debt, despite a UN

decision that a country that reaches a settlement agreement with the

majority of the creditors is not to be pressured by non-conforming

creditors. In the case of Argentina, the vulture lord bought the

country’s default debt for a pittance and now that the nation’s economy

had recovered he wants to make a fortune on the back of the population.

This is how our western fraudulent monetary system functions.

China’s economy has surpassed that of the

United States and this new eastern alliance is considered an existential

threat to the fake western economy. CIPS, already used for trading and

monetary exchange within China and Russia, is also applied by the

remaining BRICS, Brazil, India and South Africa; and by the members of

the Shanghai Cooperation Organization (SCO), plus India, Pakistan and

Iran, as well as the Eurasian Economic Union (EEU – Armenia, Belarus,

Kazakhstan, Kyrgyzstan, Russia and Tajikistan). It is said that CIPS is

ready to be launched worldwide as early as September 2016. It would be a

formidable alternative to the western dollar based monetary Ponzi

scheme.

The new eastern monetary sovereignty is

one of the major reasons why Washington tries so hard to destroy the

BRICS, mainly China and Russia – and lately with a special effort of

false accusations also Brazil through a Latin America type Color

Revolution.

In addition, the Yuan late last year was

accepted by the IMF in its SDR basket as the fifth reserve currency, the

other four being the US dollar, the British pound, the euro and the

Japanese yen. The SDR, or Special Drawing Right, functions like a

virtual currency. It is made up of the weighted average of the five

currencies and can be lent to countries at their request, as a way of

reducing exchange risks. Being part of the SDR, the yuan has become an

official reserve currency. In fact, in Asia the yuan is already heavily

used in many countries’ treasuries, as an alternative to the ever more

volatile US dollar.

It is no secret, the western dollar-led

fiat monetary system is on its last leg – as eventually any Ponzi scheme

will be. What does ‘fiat’ mean? It is money created out of thin air. It

has no backing whatsoever; not gold, not even the economic output

generated by the country or countries issuing the money, i.e. the United

States of America and Europe. It is simply declared “legal tender’’ by

Government decree.

No pyramid scheme is sustainable in the

long run and eventually will collapse. It was invented and is used by a

small invisible upper crest of elite making insane amounts of profit on

the back of the 99% of us. Since these elitists are in control of the

media with their lie propaganda, as well as the warmongering killing

machine, US armed forces, NATO, combined with the international security

and spy apparatus, CIA, MI6, Mossad, DGSE, the German Federal

Intelligence Service (BND) and more, we are powerless – but powerless

only as long as we ignore what’s really going on behind the curtain.

Our western monetary system is based on

debt has all the hallmarks of a failing global monster octopus. The US

banking system was deregulated in the 1990’s by President Clinton. The

European vassals followed suit in the early 2000’s. About 97% of all the

money in circulation in the western world is ‘made’ by private banks by

a mouse click in the form of ‘loans’ or debt. Every loan a private bank

hands out is a liability on that bank’s books; a liability that bears

interest, the key generator of the banks’ profits. Profit from thin air!

No work, no production, no real added value to the economy.

If and when the banks within this web of

debt begin recalling their outstanding liabilities, they may set a

non-stoppable avalanche in motion – leading to a chaotic end of the

system. This end-run may have just begun. We have seen a gradual

build-up since the end of WWII with the armament of the Cold War farce,

and a high point with the manufactured sub-prime crisis of 2007 / 2008 /

2009, prompting an artificial and endless global economic crisis which

may come crashing down in 2016 / 2017.

The damage may be humongous, leaving

behind chaos, poverty, famine, misery – death. With the invisible ruling

elite having cashed in, remaining on top and being liable to start

again from scratch. – If we let them. It always boils down to the same:

An uninformed people can be manipulated at will and is left in awe when

hit by unexpected events, like acts of terror by bombs or banks.

Let us be crystal clear – we are all

uninformed as long as we listen to and believe in the mainstream media –

which are controlled by six Anglo-Zionist media giants, feeding the

western public with 90% of the information, the so-called ‘news’ that we

consume so eagerly every day; the barrage of lies that repeat

themselves in every western country every hour on the hour – and, thus,

become the truth. Period.

We must get out of our comfortable

armchairs, listen to that innermost spark in the back of our minds,

telling us against all avalanches of lies that there is something wrong,

that we are being fed deception. We have to dig for the truth. And it

is there – on internet, on alternative media, like Global Research,

Information Clearing House, VNN, The Saker, NEO, Russia Today, Sputnik

News, PressTV, TeleSUR – and many more credible sources of

truth-seekers.

Back to the impending collapse. – The

ground rules for our pyramid monetary scheme have been laid in 1913 by

the creation of the FED. Again, the FED is an entirely private,

Rothschild dominated banking institution that serves as the US Central

Bank. It is the omnipotent dollar making machine. It was fraudulently

and secretly conceived in 1910 on Jekyll Island, Georgia, and described

by Jekyll Island history (http://www.jekyllislandhistory.com/federalreserve.shtml ) as the “duck hunt” which

“included Senator Nelson Aldrich, his personal secretary Arthur Shelton, former Harvard University professor of economics Dr. A. Piatt Andrew, J.P. Morgan & Co. partner Henry P. Davison, National City Bank president Frank A. Vanderlip and Kuhn, Loeb, and Co. partner Paul M. Warburg. From the start the group proceeded covertly. They began by shunning the use of their last names and met quietly at Aldrich’s private railway car in New Jersey.”

The concoction of these secretive “duck

hunters” became in 1913 the privately owned Rothschild dominated Federal

Reserve System, the US central bank by deceit.

After signing the FED act into existence, President Woodrow Wilson declared,

“I am a most unhappy man. I have unwittingly ruined my country. A great industrial nation is controlled by its system of credit. Our system of credit is concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men. We have come to be one of the worst ruled, one of the most completely controlled and dominated Governments in the civilized world no longer a Government by free opinion, no longer a Government by conviction and the vote of the majority, but a Government by the opinion and duress of a small group of dominant men.”

The Anglo-Saxon system had a central bank

in England since way back in 1694. It was then already controlled by the

Rothschilds, as was the entire banking system. Baron Nathan Mayer

Rothschild once declared:

“I care not what puppet is placed upon the throne of England to rule the Empire on which the sun never sets. The man that controls Britain’s money supply controls the British Empire, and I control the British money supply.”

The

Rothschild family’s fortune cannot be properly estimated, but it must

be in the trillions. What Baron Nathan Mayer Rothschild may have said

some 300 years ago, still holds true to this day.

The

Rothschild family’s fortune cannot be properly estimated, but it must

be in the trillions. What Baron Nathan Mayer Rothschild may have said

some 300 years ago, still holds true to this day.Global Currency Reset – New Currency for U.S. – 100% Gold-Backed by Asian Gold

Enormous amounts of Asian gold will be used to back a new U.S. Currency, and others. In return, military forces worldwide agree to cooperate to protect Planet Earth.Negotiations with the Cabal have commenced via Asian Elders of the White Dragon Society The planet’s GOLD will be used to back new currencies worldwide, and NOT the Federal Reserve currencies or bills. America will get a gold-backed dollar. Other currencies will likewise be cleaned up and backed-up. The Light Alliance is comprised of higher beings who are coordinating the (very complex currency reset) plan worldwide – -and working with local people to actually implement it. The overall goal is to reduce fear in the population, so that we can get through this 2012 transition, which is right around the corner. The timing of the latter, depends on you waking up to these worldly events. You are being taken care of, but you have to wake up to see it. Please review the videos (in this channel) in order, to understand the big picture – - and you will then understand that all of events are aimed at reducing fear so that you can successfully get thru this transition.